Category: Blog | Altius Mortgage

What Types of Income Qualify for Non-QM Mortgage Approval

5 minute read

Have you ever walked into a bank, ready to buy your dream home, only to be turned away because your…

Read MoreCategories

For older homeowners considering reverse mortgages or retirement strategies.

Includes refinance guidance, equity access, strategic debt relief.

Covers paperwork, insurance, closing logistics, rate trends, home touring, timing, and strategy.

Covers first-time buying, FHA specifics, loan choices, credit prep, and costs.

If you are unsure where to start, take a look at what our professionals are saying about the current mortgage industry!

Featured Resources

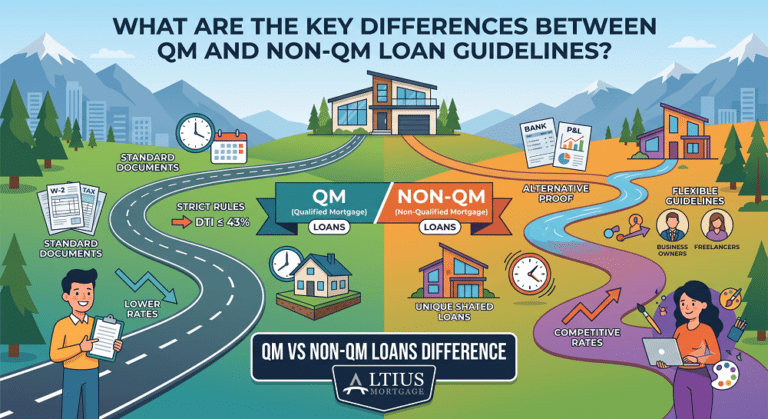

What Are the Key Differences Between QM and Non-QM Loan Guidelines

5 minute read

Navigating the mortgage market can feel like learning a new language, especially when lenders start throwing around industry acronyms. If…

Read More

What to Expect During the Non-QM Loan Approval Process

5 minute read

The modern workforce has changed dramatically, especially here in Utah’s thriving Silicon Slopes. Today, more professionals are stepping away from…

Read More

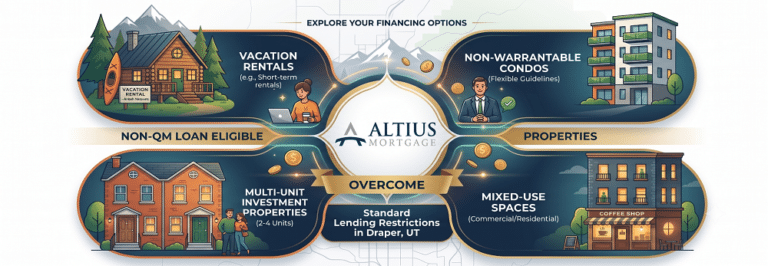

What Types of Properties Can Be Financed Using Non-QM Loans

5 minute read

If you are hunting for real estate in the fast-paced Utah market, you might have already run into the strict,…

Read More

How to Buy a Home in Utah With Little or No Down Payment

4 minute read

For many aspiring homeowners in the Beehive State, the dream of homeownership feels just out of reach due to the…

Read More

What Role Location Plays in Down Payment Assistance Eligibility

5 minute read

Buying a home is one of life’s most significant milestones. While the excitement of finding the perfect property in Utah…

Read More

How Rising Home Prices Affect Down Payment Assistance Needs

5 minute read

Buying a home is one of the most significant financial milestones in life, especially here in Utah. Whether you are…

Read More