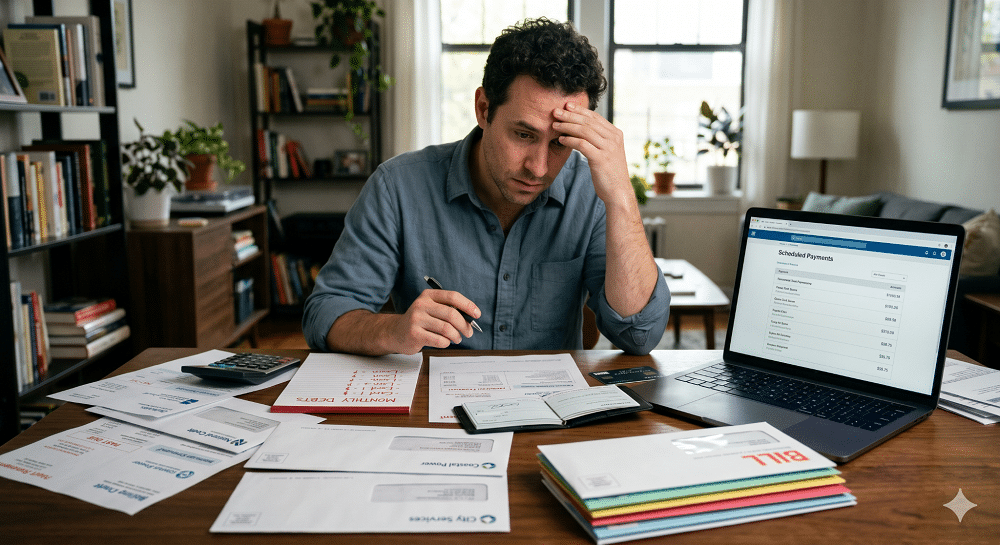

How to Simplify Multiple Debt Payments Without Increasing Risk

Managing multiple monthly debt payments can feel like a high-wire act, particularly when balancing standard household expenses with your long-term financial goals. For many residents of Draper, Utah, the pressure of a shifting housing market—where rising home prices have driven up initial costs for buyers—can make the burden of existing debt feel even heavier. When monthly bills from credit cards, student loans, and auto financing start to stack up, the stress can impact your ability to qualify for major life investments, such as a new home purchase.

Finding a path to debt consolidation without risk is not just about moving numbers around on a spreadsheet; it is about creating a stable, predictable financial environment that protects your future assets while easing your current burden.

The Impact of Modern Financial Pressures

Before addressing debt management, it is important to recognize the external factors complicating financial stability. In the current market, affordability pressure is real. Higher home prices have inevitably increased the upfront costs for buyers, from larger down payments to higher closing costs.

Because of these price surges, more buyers than ever are relying on government-backed assistance programs. Agencies are responding to this reality by expanding funding availability and frequently revising eligibility requirements to keep homeownership accessible. However, these programs are often limited in scope. If you are planning to utilize assistance, early action is crucial. Applying early—before funds are exhausted—can be the difference between securing the necessary support and being forced to delay your home-buying plans. Understanding this landscape is the first step in managing your debt because a clear picture of your total financial commitment allows you to make informed decisions about whether to consolidate now or focus on debt reduction first.

Understanding Debt Consolidation

Debt consolidation essentially involves rolling multiple high-interest or scattered debts into a single, more manageable monthly payment. Done correctly, it can simplify your cash flow and potentially reduce the amount of interest paid over time.

However, the “without risk” component is where many borrowers struggle. The risk often comes from two sources: extending the repayment term significantly (which can increase the total interest paid over the life of the loan) or utilizing collateral—like your home—to secure a lower-interest debt consolidation loan. If that loan is not managed carefully, you may be putting your home at risk.

To achieve debt consolidation without risk, consider these strategies:

- Focus on Fixed Rates: Whenever possible, choose consolidation options with fixed interest rates. A fixed payment provides predictability, shielding your budget from the volatility of market-driven interest rate hikes.

- Avoid Extending Terms Beyond Necessity: While lowering your monthly payment by spreading it out over 20 or 30 years sounds appealing, it often results in paying significantly more in total interest. Aim for a term that lowers your monthly payment enough to breathe, but is short enough to clear the debt efficiently.

- Prioritize Debt Repayment Habits: Consolidation is a tool, not a cure. If you do not change the spending patterns that led to the multiple debt payments in the first place, you risk running up the same balances again while still paying off the consolidation loan.

The Role of Professional Guidance

In a competitive financial environment like Utah, working with a mortgage professional who understands both local market dynamics and broader debt management strategies can provide a distinct advantage. An experienced mortgage expert can help you assess your debt-to-income (DTI) ratio—a critical number that lenders look at to determine your borrowing capacity.

If your DTI is currently too high due to multiple payments, a professional can help you evaluate whether consolidating those debts will actually improve your profile for future mortgage applications or if other strategies are more appropriate. They can also explain the nuance between unsecured personal loans for debt consolidation and equity-based products, ensuring you understand the implications of each before you sign any agreements.

Stability

Simplifying your financial life should reduce your stress, not increase your risk. By addressing affordability pressures early, keeping a close eye on your DTI, and focusing on fixed, predictable consolidation strategies, you can clear the path for your future goals—whether that is buying your first home in Draper or upgrading to a property that better suits your growing family.

Take control of your financial narrative. By acting with foresight and choosing strategies that prioritize long-term stability over short-term relief, you can successfully simplify your debt and move forward with confidence.

Contact us today to learn more!